Spaced Out: Tight availability shifts leverage back to landlords

Early 2025 was a positive time for retailers looking to expand their footprints, but things have since reverted back to a landlord’s market.

Notable bankruptcy filings of late 2024 and early 2025 included Party City, Joann, Big Lots, Forever 21 and others, and provided a much-needed 12.5 million square feet of retail space to the commercial market at the beginning of last year, according to CoStar’s data at the time.

The wave of new space was quickly snapped up by expanding retailers, and while the financial health of struggling chains is always being monitored, experts say that large-scale availability won’t be seen again in the near future.

“Distressed activities opened a door and created some efficiencies for retailers to be able to try to win those spaces,” said Al Williams, co-head, North American real estate services, Gordon Brothers. “Some retailers were good at it, while some were a little late to the game. We haven’t seen as many of those bankruptcies this year, and likely won’t, because of the natural ebb and flow.”

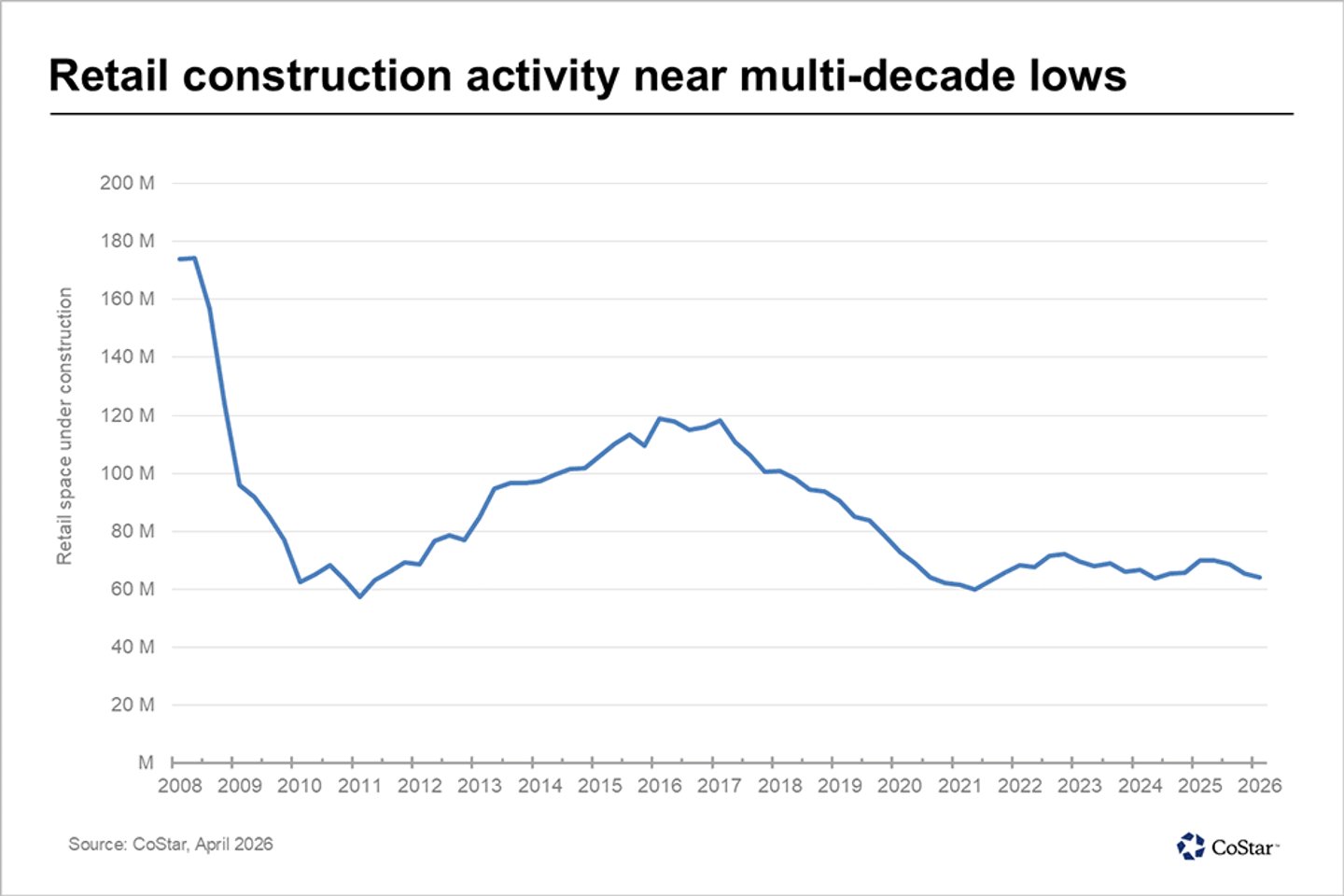

While bankruptcies have subsided, new retail construction continues to lag from past levels, including 2025. In the first quarter of 2026, roughly 64.2 million square feet of retail space was under construction in the United States, down from approximately 70 million square feet compared to the same quarter last year, according to CoStar. This figure is well below the 10-year average, which consistently exceeded 90 million square feet.

The lack of construction is leading to highly restricted available space. According to the Crexi National Commercial Real Estate Report for March 2026, retail vacancy held steady at 5.2%, unchanged from February, and 210 basis points below the 7.3% vacancy rate recorded a year ago, making retail one of the tightest asset classes in Crexi’s data.

The average sale price for retail properties on Crexi came in at $217.88 per square foot in March 2026, an 11.9% decline from $247.38 in February, but still 8.3% above its March 2025 level of $199.65 per square foot. Despite the month-to-month drop, the average asking price rose to $335.17 per square foot in March, up 5.2% from February and a notable 24.3% above year-ago levels.

“Rent growth and competition for quality real estate is going to continue, especially with the limited supply,” said Williams. “Landlords are in a stronger position, and the best space is going to be increasingly competitive.”

Global pressures taking a toll

To make matters more difficult for retailers looking to grow and developers looking to meet demand, import tariffs implemented by President Donald Trump have increased the prices of construction materials across the board.

Despite a recent Supreme Court ruling that struck down Trump’s sweeping April 2, 2025 “Liberation Day” tariff agenda, the administration has since invoked Section 122 of the Trade Act of 1974, imposing a 10% across-the-board import surcharge on goods from nearly all countries. This surcharge expires after 150 days, on July 24, 2026, unless Congress votes to extend it, according to the Atlantic Council’s Trump Tariff Tracker.

“The biggest thing impacting new construction now is import tariffs,” said Michael Burden, co-head, North American real estate services, Gordon Brothers. “You have the post-pandemic interest rate increase, and you have the unknown of what’s happening in the Middle East that will keep us in the cycle of limited new construction.”

The United States and Israel’s attacks on Iran that began in late February have led to a worldwide spike in oil prices and the on-and-off closure of the Strait of Hormuz, one of the globe’s most important corridors for energy transportation, making things look even bleaker when it comes to the prospects of new construction.

While negotiations to end the conflict diplomatically have been underway in recent weeks, the effects are already being felt. Surging prices in oil and natural gas drove up overall construction input prices (which includes energy, materials and equipment) in March, increasing 2.2% compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics Producer Price Index data.

Overall construction input prices in March were 4.8% higher than one year ago. The biggest increase seen in March was in crude petroleum, for which prices rose 20.2%.

“The increase we are already seeing in transportation costs is going to really hurt a lot of goods-based retailers,” said Brandon Svec, national director of U.S. retail analytics at CoStar. “I think the outlook for the 2026 retail market is more bearish today than it was two months ago. There’s really no other way to get around the fuel and transportation costs.”

In-demand markets, in-demand tenants

One thing that hasn’t changed much from last year is that when new construction is being built, the Sunbelt continues to lead the way nationwide.

CoStar data from the first quarter shows that Dallas, Austin and Houston were the only three markets with more than 3 million square feet of space under construction. Phoenix was not far behind, with more than 2.5 million square feet under construction.

Other Sunbelt cities including Las Vegas, Charlotte, N.C., Atlanta and Orlando all exceeded 1 million square feet of new construction as of April. Chicago was the only outlier city to reach this new development threshold.

Fueled by growing populations post-pandemic, retailers are willing to pay for ground-up construction in the Sunbelt to meet consumer demands, in addition to forking over more in rent at existing retail centers.

“In Phoenix in particular, retail is very strong right now,” said Jeff Axtell, executive VP of development at Vestar, which has been more active than most when it comes to ground-up construction. “In the past seven to 10 years, over a million people have moved into Phoenix, and very little new supply came online. The supply and vacancies are really low, and rents are increasing very well for the landlords.”

Despite costs increasing across the board when it comes to new developments, Axtell added that in select markets, it still makes sense for retail’s major players to pay more today for newly built space to enjoy future sales growth tomorrow.

“Tenants are realizing that in order for them to meet their Wall Street projections for the number of the stores that they want to open and to grow their sales, they will have to pay higher rents to get the available stores,” he said. “The retailers are willing to pay the rent that we need to cover the construction cost increases that we’ve seen in the past five to 10 years.”

In addition to the Sunbelt’s continued success, another constant from last year is the type of retailers that are continuing to look toward expansion.

Discount retailers are thriving as consumers see increased prices, especially in recent months. In the first quarter of the year, discount’s heaviest hitters all announced expansion plans, with Dollar General and Family Dollar also announcing plans to test new store formats while growing their footprints.

“Off-price and discount are definitely still winning,” said Svec. "Dollar General and Dollar Tree are rapidly expanding, along with TJX, Ross and Five Below. The consumer’s focus on value remains fully intact, and that continues to be a tailwind for retail demand for those value-oriented retailers.”

Patrick Nutt, senior managing principal & co-head of National Net Lease at SRS Real Estate Partners, said that the “K-shaped economy” will only continue to benefit off-price and discount retailers’ balance sheets, and in turn, fuel their expansion efforts.

“When it comes to the junior box and bigger box spaces, TJX and Ross are the first to get there,” said Nutt. “Five Below just had a tremendous quarter. The retailers you are familiar with in the box space are the ones who are continuing to absorb it.”

Health and wellness-focused retailers and fitness chains are also among the tenants snapping up space in retail centers. Despite cost pressures, consumers are still prioritizing their physical and mental well-being, and landlords can benefit from the foot traffic and stability that a gym or boutique fitness chain can add to a shopping center.

“We’ve seen leasing by fitness centers and health-oriented operators really accelerate over the last year,” added Svec. “I would say fitness has been the one of the unsung heroes of backfill, especially of Class B and C spaces they can grab at lower rents.”

Crunch Fitness president Chequan Lewis said that the chain plans to open 100 new locations in 2026, with second-generation retail space playing a key role in expansion plans.

“One of the most exciting things happening in fitness real estate right now is adaptive reuse,” he said. “We’re converting second- and third-generation retail spaces into gyms. It makes so much sense – lower build-out costs, already in high-traffic locations, and familiar to the consumers we’re trying to reach.”

Quick-serve and fast-casual restaurant chains have also been impacted by the lack of new construction. However, these categories are more flexible with the store size they can take advantage of, which benefits real estate operators looking to add a traffic-driving food and beverage tenant to a retail property.

“Single-tenant buildings like an old Burger King and Wendy’s might have been 3,000 to 4,000 square feet, but most of the new QSR concepts today can deal with 600 to 1,000 square feet,” noted Nutt. “National brands like Starbucks, Dutch Bros and Chick-fil-A are also doing drive-thru only concepts, along with new and emerging brands like Swig, 7 Brew and Salad and Go.”

Consumer strain

While fighting for available real estate space to expand into, retailers are increasingly conscious of consumer sentiment, which has taken a nosedive recently amid spiking fuel prices.

The University of Michigan’s Index of Consumer Sentiment’s preliminary reading for April fell to 47.6, down 10.7% from March, extending a decline that began with the start of the Iran conflict.

Year-ahead inflation expectations from the index rose from 3.8% in March to 4.8% in early April, the largest one-month increase since April 2025. The current reading exceeds those seen in 2024 and remains well above the 2.3 to 3.0% range seen in the two years pre-pandemic.

Consumer strain is felt most directly at gas pumps. According to AAA, the national average price of a gallon of gasoline has increased nearly a dollar compared to last spring.

“The longer the Iran conflict goes on, the greater the magnitude of the effects,” said Svec. “Consumers are having to reallocate wallet share towards the pump and away from other discretionary categories, and that discretionary spending was already thin.”

Nutt added that consumer pullback due to prolonged high gas prices will have an impact on even the retailers that serve lower-income shoppers.

“If you look at the consumer today from a macroeconomic perspective, we are very much in a K-shaped economy,” said Nutt. “The higher end of the K shape will continue to spend and absorb the inflation hits. I do worry about the bottom half of the consumer, those that are truly very price conscious.”

With prices expected to continue pinching consumers for the foreseeable future, retail center operators should prioritize offering guests value beyond shopping amenities, according to Paul Ghermezian, senior VP of megamall owner and operator Triple Five Group.

At Mall of America and American Dream, entertainment programming is routine in an effort to offer guests a unique and enjoyable experience beyond just shopping. Later this spring, American Dream will open the 3,000-seat Dream Live Performing Arts Center, which will host a wide range of events, including theater and dance productions, comedy shows and live concerts.

“Consumers are willing to spend on things that give them more than just material value,” said Ghermezian. “They want to come out and have a positive experience with family or friends. We’re all very conscious of economics. When a customer comes in and they do have those dollars to spend, we want them to be getting something meaningful.”

Looking ahead

The future may seem uncertain for retailers and consumers alike given the impact of geopolitical tensions. Still, there is a sense of cautious optimism among some commercial real estate professionals, as economic downturns have been weathered in the past and are a part of retail’s natural evolution.

“It’s easy to look at a situation and say ‘oh, this is new,’ but there’s always elements that come together and drive challenges,” said Williams. “At the end of the day, the retailers that are growing now have working models that can probably weather this. Things inevitably change, but they will stick to their game plan for the most part.”

Nutt added that not all retailers may handle a prolonged economic downturn the same way, noting that legacy brands may be more susceptible to curbed consumer spending, while newer brands may be better positioned to weather it.

“There are a lot of brands that can survive a temporary downturn, whether it happens for a month or a quarter, but I think there are some that are holding on for dear life,” he said. “They are paying their bills as they get the money coming in, and when the consumer slows down just a little bit, I think that could be detrimental to them.”

When it comes to retail expansion, second generation space remains the most cost-effective vehicle for growth, and will likely be so for the foreseeable future.

“More than ever, retailers in growth mode are going to have to look at second-generation space,” said Burden. “They are going to have to dive into areas that they haven’t typically grown in the past, such as taking advantage of a company’s distress, and try and grow through those channels rather than just waiting for developers to build new centers.”