Open for Business: Available retail space hits recent high

Though new construction of retail real estate space continues to remain at low levels, space availability received an adrenaline shot in the first quarter of 2025.

Commercial real estate data firm CoStar Group revealed in a recent report that available retail space has increased by approximately 12.5 million sq. ft. since the start of the year. Fueled by high-profile store closures, which more than doubled in 2024 compared to 2023, availability reached 4.8% as of March, the most retail space available for lease than at any point in the past two years.

A changing economic environment has led to a diverse list of retailers to close hundreds of stores or shut down operations entirely. Outside of the notable retail casualties of Big Lots, Joann, and Forever 21, chains including Dollar General, Macy’s, JCPenney, and GameStop have all announced plans to close stores this year.

“Overall, higher occupancy costs, higher labor costs, and higher costs from suppliers are making for a tougher landscape,” said Brandon Svec, national director of U.S. retail analytics at CoStar. “Some of it is the shifting consumption profile within the economy today. Consumers are really pushing more towards essential purchases and away from discretionary purchases, especially those consumers in the bottom 80% or so of the income bracket.”

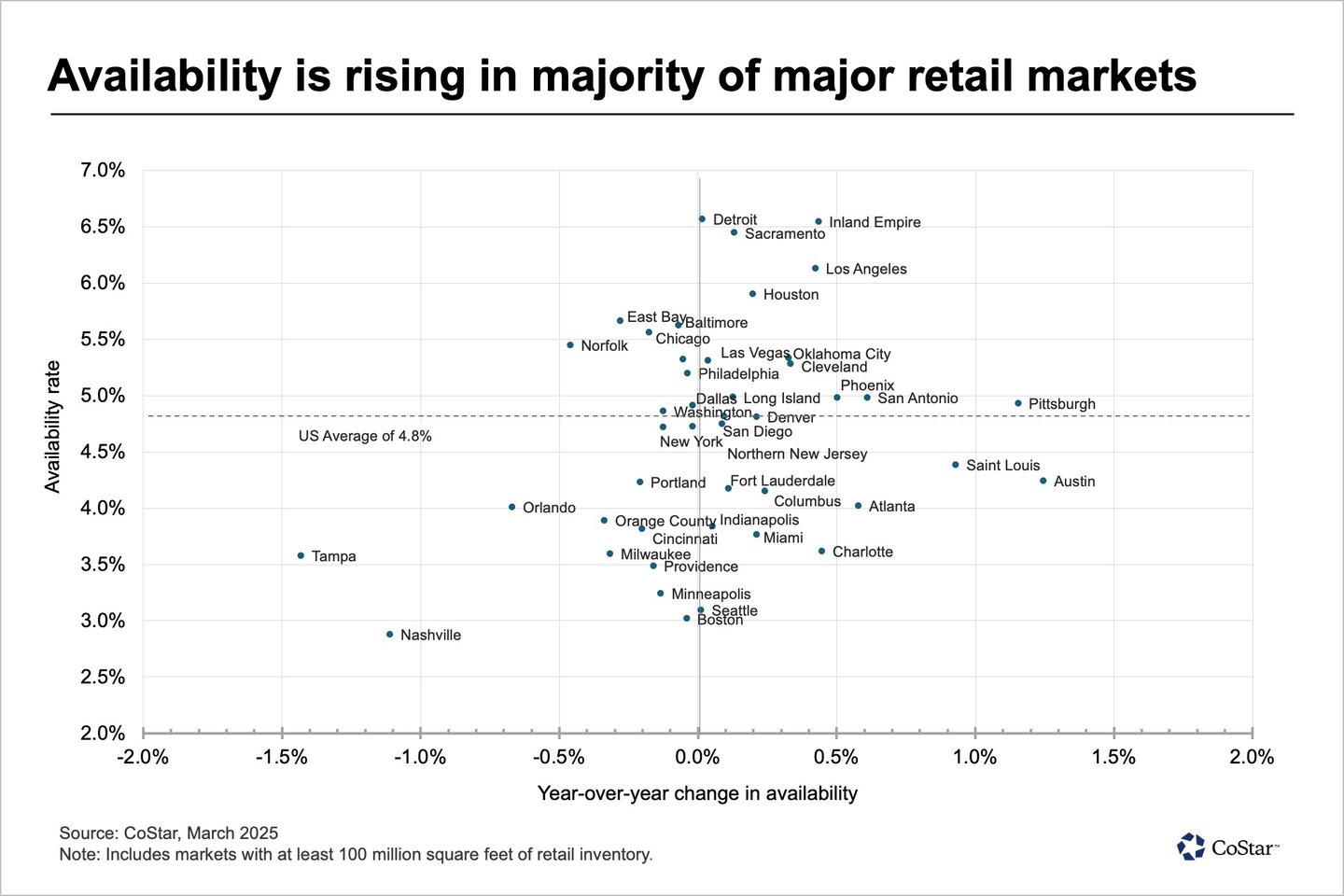

The increase in retail spaces has been seen across the United States, but some markets are seeing greater rises than others. Of the 143 U.S. markets within the CoStar national retail index, available retail space increased in 79 over the past year, while 64 saw a decline in retail space availability over the same time frame.

In comparison, in the first quarter of 2024, only 58 of the 143 markets increased retail space availability over the prior year, while 85 saw availability decline. Among the 44 major U.S. retail markets, defined as those with at least 100 million sq. ft. of retail space, availability increased in 24 of them over the past year. As of March 2025, the U.S. average availability rate was 4.8%.

Austin, Texas, Pittsburgh, and St. Louis saw the highest year-over-year increases in availability, while fast-growing cities such as Tampa, Fla., Nashville, Tenn., and Orlando, Fla., saw avail- ability decrease the most. Detroit and key California markets (Inland Empire, Los Angeles, and Sacramento) had the highest overall availability rates.

When it comes to what size properties are becoming available, CoStar found that large boxes, including those formerly occupied by chains such as Big Lots and Joann, are leading the increase. For the first quarter of 2025, spaces of 25,000 sq. ft. or more saw a 12.9% increase in availability compared to the first quarter of 2024.

Spaces between 10,000 and 24,999 sq. ft. saw a 9.3% increase in the period, and spaces between 5,000 and 9,999 sq. ft. saw a 3.0% increase. The beginning of 2025 marked the fourth-straight quarter of increased availability for these large properties.

Construction

Retail construction has remained consistently low for seven years, according to a recent report from Cushman & Wakefield, contributing to low vacancy rates, even as store closures mounted last year. And it hasn’t been just retail impacted by higher interest rates, material inflation, and labor costs.

Industrial and multifamily construction pipelines have dropped below first quarter of 2020 levels by 17% and 8%, respectively, and office development, at record highs in 2020, has declined significantly from 135 million sq. ft. to under 30 million sq. ft.

“Store closures have primarily fallen on Class B properties,” said Svec. “The Joanns, the Party Citys — all of these will provide a wave of supply. New construction is almost nonexistent. Costs overall are a hard hurdle to overcome on ground-up construction.”

A recent report from CBRE further proved the fact of increasing large space availability. Georgia, part of the fast-growing Sun Belt region, saw available anchor space increase by a whopping 57% in 2024. At the end of last year, there was 6.8 million sq. ft. of anchor space available spread across 151 properties, compared to 4.3 million sq. ft. at the end of 2023.

Joe Parrott, senior VP of retail services at CBRE, said that the closures of chains such as Conn’s and Bargain Hunt disproportionately impacted availability in the South and Southeast. Conn’s closed more than 553 locations across its two banners, while Bargain Hunt closed 92 stores.

“Those, combined with the big national chains like Big Lots, American Freight, and Joann that went under, Georgia was affected by all of them,” he said. “Whereas the West or Northeast didn’t have all of those closures.”

Who will fill new available spaces?

As to the next tenants that could fill vacant retail space, it appears that grocers, restaurants, and specialty retailers are the most primed for success.

According to Datex Property Solutions’ Tenant Track for 2025, categories with the highest six-year sales per sq. ft. averages were grocery chains ($597), beauty retailers ($686), fast-food chains ($673), restaurants ($583), and sporting goods retailers ($339). Drug stores, specialty food chains, pet retailers, and dollar stores have seen their merchant health move in the opposite direction over the same period.

“Certain merchant categories disproportionately benefited from the pandemic and others were adversely affected,” said Mark Sigal, CEO of Datex. “Until recently, there’s been a dearth of available space for the merchants and merchant categories that are expanding.”

CBRE’s report noted that amid high-profile store closures, some categories are ready to expand into the bigger Class B and C spaces. Fitness and recreation tenants filled 20% of available anchor space in Georgia, followed by apparel and shoes (16%), and furniture and decor (14%).

“The chains in categories that are profitable and have cash on hand are looking to grow,” added Parrott, noting that increased availability will mean greater competition for both retailers looking to expand and property owners alike.

“Prior to this recent spate of liquidations, it had become much more of a landlord’s market than the historical norm,” he said. “Now we’ve reached a healthy market equilibrium.”

Competition among tenants for quality space is fierce, added Perrott, but owners of lower-quality space are now having to compete for tenants.

“We’re seeing a widening of the rent gap between quality spaces and secondary spaces, and I think that’s going to widen further,” he said.

R.J. Hottovy, head of analytical research at retail data firm Placer.ai, noted that just as changing consumer behavior led to store closures for some already challenged retailers, it will also have an impact on which chains will fill vacant spaces in B and C centers.

“There’s been a shift to mass merchants, which certainly has put some pressure on these retailers [that have closed stores], and certainly online retailers put some downward pressure on them,” said Hottovy. “A consistent theme of off-price and a ‘treasure hunt’ atmosphere has been very popular – low prices but unique products is a recipe that’s worked very well in this environment.”

As an example, Hottovy noted that private label and value grocers such as Aldi and Lidl have been very disruptive in taking visits from traditional grocers.

Hottovy added that while off-price apparel chains such as TJ Maxx and Ross are expanding their footprint in large open spaces, service businesses like massage, hair, and nail salons are filling smaller open spaces at shopping centers.

Successful fast-casual and quick-serve chains are growing as well, and despite high construction costs, some properties are building new structures to accommodate restaurants where possible.

“Some of these B and C locations are adding pad locations in the parking lots, and we’re seeing some of the chicken chains and coffee chains take that space,” Hottovy noted.

Investments and redevelopments at newer properties in better locations will also have an impact on how managers of Class B and C properties attempt to diversify their tenant mix while filling spaces. Mixed-use developments bringing housing, entertainment options, and lifestyle amenities to Class A centers will push out some tenants, and force B and C properties to get more creative to compete for foot traffic.

“All it takes is one new tenant to change the fortune of a property,” said Hottovy. “Mall operators are going to look to non-traditional tenants. That is going to be an interesting thing to look at — not just this year, but over the next couple of years.”

Will rents decrease with more availability?

According to the Datex report, retail rents increased only slightly (2.79%) in 2024, even as store closures increased throughout the year. Experts say that given the severe lack of new construction, rents likely won’t decrease across the board, but could in select areas.

CoStar’s Svec said that clustered vacancies will likely reduce the ability of landlords to increase rents at the same rate as the rest of the market, as new tenants will be competing with multiple other vacancies nearby.

“We are at a historic low for space, and nearly two-thirds of that space is B or C, so when we think about the higher quality opportunities, there just really aren’t a lot out there,” said Svec. “We are going to see rental growth slow in the areas where availability stacks up on top of each other. If you have a Joann, and a Big Lots, and a Party City, and all three are sitting vacant, that is certainly going to impact rents around that area on the larger boxes, but not as much on the smaller spaces.”

CBRE’s Georgia report showed a slight decrease in both average asking rents and average rent comps from 2023 to 2024.

"There’s two kinds of tenants out there: the ones that are seeking the best quality space, and the ones that are looking for the best deal,” said Parrott. “The ones looking for the deals are going to find more opportunities to expand this year.”

Parrott added that more deal-oriented rental agreements will take place this year, which will pull the average rent caps down, but will not be reflective of declining rates across the board on comparable space.

What’s next?

The spate of store closures has enlivened the ever-changing retail landscape. The good news for expanding retailers, however, is that some expect the closures to continue — especially as new tariffs begin to impact the global economy.

“We expect store closures to continue through the remainder of 2025, and at a pace that will outstrip the rate at which retailers are backfilling space,” said Al Williams and Michael Burden, co-heads of North American real estate services at Gordon Brothers, in a written reply to questions posed by Chain Store Age. “While select categories, particularly discount and service-based retailers, are expanding, overall absorption remains uneven. That said, the leasing market is showing real resilience in high-demand trade areas.”

Despite tough economic times, there is a potential bright side to store downsizing. Experts say retailers closing stores can potentially benefit both retailers looking to right-size, and property managers looking to bring new tenants – and life – to a property.

“Store closures can kind of get negative headlines, but in a lot of cases, it’s a good thing for some of these retailers,” said Hottovy. “We’ve seen such a shift in migration, and we’ve seen changes in consumer behavior. In some cases, store closures are necessary to make a stronger store portfolio.”