Annual Store Construction & Outfitting Survey

Although the uncertain economy continues to take a toll on store development, retailers’ expansion and remodeling plans are beginning to creep up, according

The exclusive survey was conducted by Leo J. Shapiro & Associates, Chicago, which compiled results from chains across the nation. The study looked at such items as expansion and remodel plans; construction costs; store size; energy costs; and costs of store-fitting and support systems, including flooring, lighting, roofing, signage, fixtures and heating, ventilation and air-conditioning.

The retailers that participated in the survey were grouped into five different segments: supermarkets, convenience stores, specialty apparel, big box (includes department stores) and home centers.

Among the participating supermarkets were Winn-Dixie Stores, Roche Bros. Supermarkets, Giant Food, Price Chopper and Acme Markets. The convenience store group included 7-Eleven, Circle K, and Stewart’s Shops.

The specialty apparel segment was represented by such chains as Abercrombie & Fitch, Jos. A Bank, The Wet Seal, Tommy Bahama and Cato Corp. The big-box category included J.C. Penney, Macy’s, OfficeMax, REI and Duckwell-Alco. Participating home centers included Lowe’s, The Andersons, True Value Co. and Riggs Building Supplies and Home Centers.

Overall, the survey polled retailers whose stores produced combined annual revenues of $153.4 billion last year. The chains that participate in the survey vary from year to year.

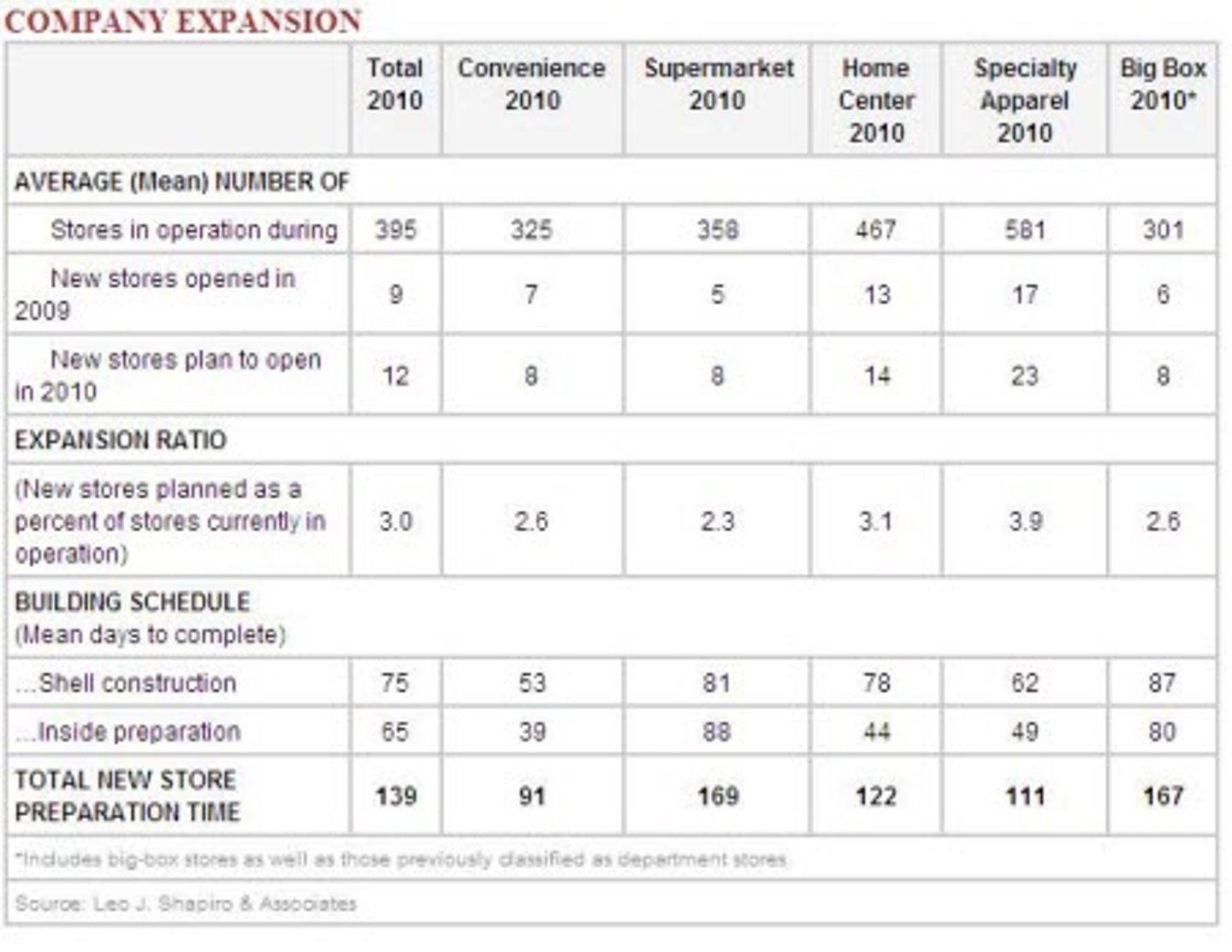

EXPANSION: For all retailers surveyed, the average number of store openings planned for 2010 was 12 (per chain), up from nine in 2009. (The comparisons regarding store-expansion plans are based on information collected in this year’s survey.)

Looking at the individual sectors, specialty stores plan to open an average of 23 stores per chain in 2010, up from 17 in 2009. Home centers plan to open 14, compared with 13, while big-box stores, supermarkets and convenience stores all plan to open eight.

The planned expansion ratio (new stores planned as a percentage of stores currently in operation) averaged 3% for all retailers, which mirrored last year’s results. Specialty stores, at 3.9%, had the greatest expansion rate among all retail categories.

Looking at expansion in a slightly different way, 50% of all retailers surveyed reported they planned to scale back on new construction in 2010. In comparison, 67.7% of all retailers in last year’s survey said they planned to cut back.

In a surprising turnaround, only 30.8% of specialty apparel retailers said they were cutting back this year. Last year, the specialty apparel group registered the biggest decline, with 84.6% scaling back. This year, the biggest cutback in expansion was reported by supermarkets, with 61.5% scaling back, followed by big-box stores at 55.6%.

The survey also revealed an uptick in retailers’ plans to remodel. Of all retailers surveyed, 35% said they were pulling back on remodeling or retrofitting initiatives. By comparison, in 2009, 50% said they were scaling back on the same.

COSTS: Construction costs were divided into two separate categories: building-shell construction costs for freestanding locations, and tenant fitout costs for stores in malls and other types of centers.

In the freestanding category, construction costs (includes concrete, structural steel, structured masonry, roof and HVAC, but excludes interior fitout) averaged $50.21 per square foot for all retailers surveyed.

Specialty apparel had the highest building costs, at $55.00 per square foot, followed by convenience stores at $52.88 per square foot.

Home centers averaged $50.33 per square foot, and supermarkets came in at $49.71 per square foot. Big-box stores had the lowest building costs, at $45.60. Costs for tenant fit-out work (includes drywall, ceiling, floor, wall finishes and interior construction, but excludes fixtures) averaged $37.36 per square foot for all retailers surveyed. Convenience stores had the highest costs at $55.00 per square foot, followed by specialty apparel, at $43.00 per square foot.

Big-box stores averaged $34.38 per square foot. Supermarkets had the lowest costs, at $31.56 per square foot.

STORE SIZE: For all retailers surveyed, new stores (defined as locations opened during the past 12 months) averaged 38,565 gross sq. ft. versus an average of 39,500 gross sq. ft. for existing units.

Among the retailers with smaller footprints were home centers, where new outlets averaged 36,875 gross sq. ft. compared with 47,914 gross sq. ft. on average, and big-box stores, whose new locations averaged 62,206 sq. ft. versus 71,250 sq. ft. for existing units. Specialty apparel held steady, at 5,769 sq. ft.

Not all retailers are building smaller. In the supermarket category, new stores averaged 63,333 sq. ft. compared with 51,923 sq. ft. for existing units. Convenience stores also increased their footprint. New stores averaged 5,313 sq. ft., up from 5,000 per sq. ft. for existing stores.

OUTFITTING COSTS: On average, store-outfitting costs were up across the board in every category when compared with last year’s results (see chart, page 52). Display fixtures retained their longstanding status as the most expensive category, averaging $8.14 per square foot for all retailers surveyed, up from $7.65 last year.

Flooring was the second most costly store-outfitting category, averaging $3.17 per square foot for all retailers surveyed, up from $2.78 per square foot last year. It was followed by interior lighting at $2.94 per square foot, up from $2.54.

Retailers on average spent $2.76 per square foot on roofing, as compared with $2.68 in last year’s survey. HVAC averaged $2.04 per square foot, up from $1.63 in last year’s results.

The least expensive store-outfitting categories were exterior signage at $1.35 per square foot, up from $1.18 per square foot last year, and interior signage, which averaged $0.82 per square foot., up from $0.66.

The survey also provided detail on the types of systems used by retailers. In the lighting category, for example, fluorescent lighting is most common, used by 96.7% on average by all retailers surveyed. For more information on the systems used by retailers, go to chainstoreage.com and look under Industry Data.

ENERGY COSTS: Energy costs continue to rise, according to survey results, averaging $2.22 per square foot for all chains surveyed, up from $1.94 on average in last year’s survey.

Specialty stores registered the highest energy expenditures, at $2.92 per square foot, followed by supermarkets at $2.84 and big-box stores at $1.82.

Energy costs were lowest for convenience stores at $1.64 per square foot and home centers at $1.38 per square foot.

GREEN: Retailers’ interest in building green continues to rise, with 81.7% of all chains surveyed reporting they use environmentally friendly materials/processes, up from 77.4% last year.

The use of green materials was strongest in the supermarket category, with 100% of all retailers on board (similar to last year’s results).

Of the home centers surveyed, 83.3% reported they were using green materials, followed by big-box stores (77.8%), specialty apparel (76.9%) and convenience stores (70%).