CoStar: Retail rent growth slows to 1.9% in Q1

After booming post-pandemic, retail rent growth is continuing to moderate.

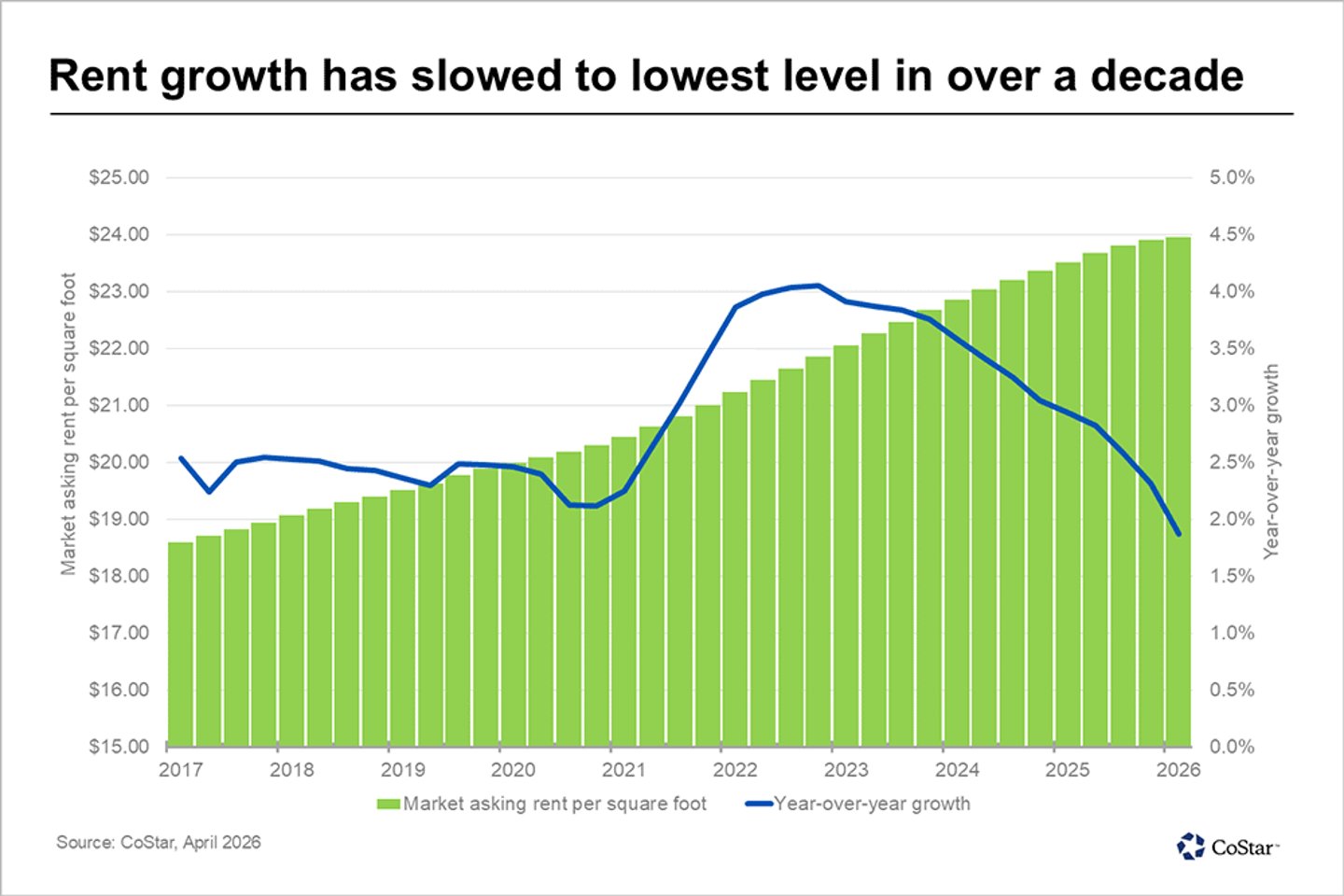

According to a new report from CoStar Group, U.S. retail asking rent growth slowed to 1.9% year over year in the first quarter of 2026, extending a downward trend that began in 2024.

The asking rent growth deceleration is seen across most major markets, though performance continues to vary by region, according to CoStar. Several Sunbelt markets that led rent growth earlier in the cycle, including Phoenix, Orlando, Atlanta, and Charlotte, still posted solid year-over-year gains at the end of the first quarter, but growth rates have slowed as asking rents plateau.

Earlier this month, CoStar data revealed that in the first quarter of 2026, roughly 64.2 million square feet of retail space was under construction in the U.S., down from approximately 70 million square feet a year earlier. The first quarter total was also well below the 10-year average, which consistently exceeded 90 million square feet.

“While U.S. retail fundamentals remain healthy, a slight loosening in vacancy alongside moderating tenant sales growth has reduced landlords’ ability to push rents at the pace seen immediately after the pandemic,” said Brandon Svec, national director of retail analytics at CoStar Group. “This slowdown is less of a sign of weakening demand than a function of normalization. As sales growth has leveled out across most retail segments, occupancy costs have risen back to pre-pandemic norms.”

Select markets, especially those in Midwestern markets, are bucking the trend, however. Minneapolis posted the strongest year over year rent gains nationally, at 6.9%, with Columbus (6.3%), St. Louis (4.1%), Milwaukee (3.8%), Cincinnati (3.3%) and Kansas City (3.1%) also ranking among the better performing markets located outside of the Sunbelt.

[READ MORE: CoStar: U.S. retail vacancy expected to rise ‘minimally’ in first half of 2026]

“With rent-to-sales ratios now more closely aligned with historical averages, and operating costs and interest rates remaining elevated, tenants have become more resistant to additional rent pressure, particularly in discretionary categories,” added Svec. “As a result, asking rent growth has moderated even as leasing activity and occupancy remain relatively strong.”