Aldi, Lidl continue gaining visitors, but different ones

As cost pressures continue to stretch consumers’ finances, discount grocers Aldi and Lidl have maintained a strong growth trajectory in the United States.

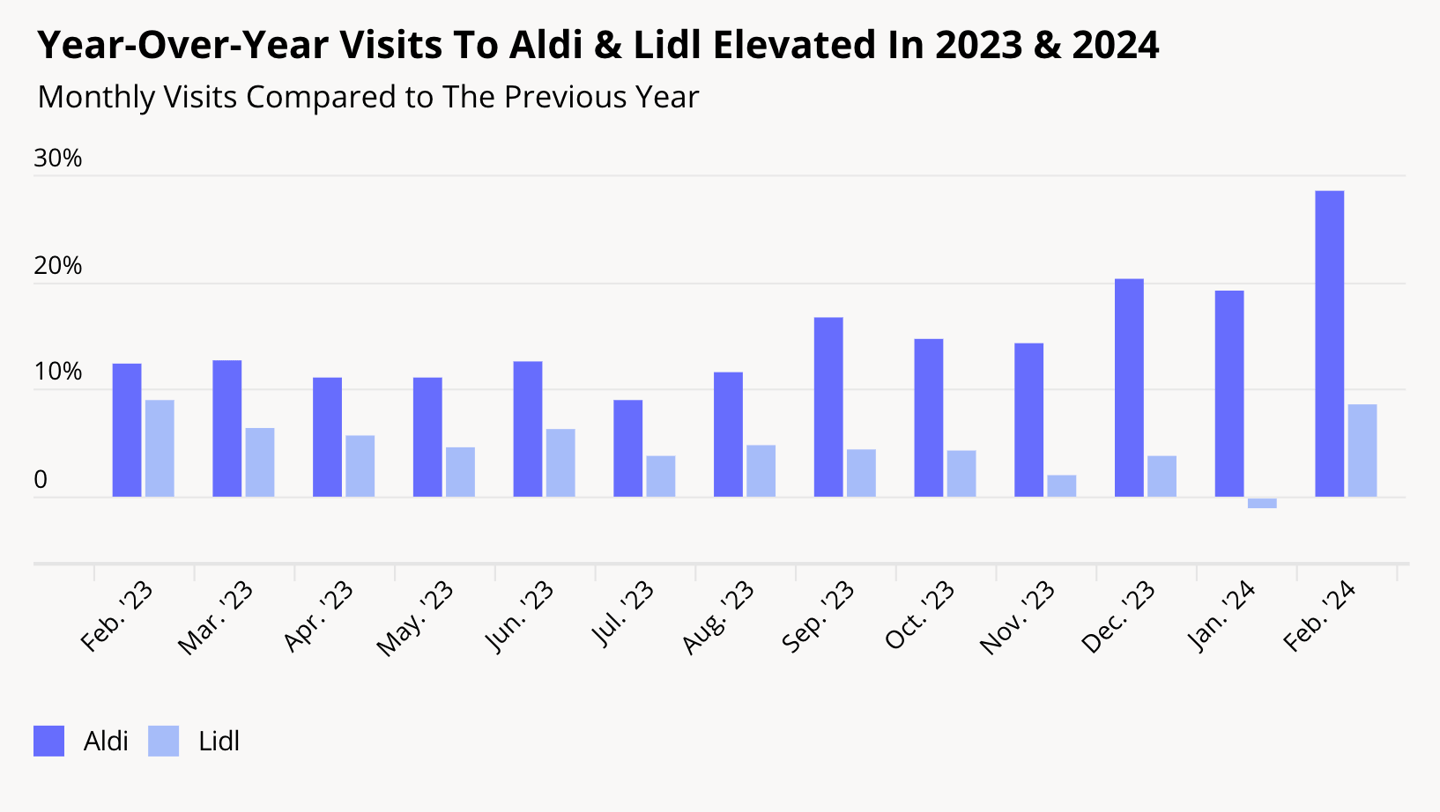

According to recent data from the foot traffic analytics provider Placer.ai, the two German founded chains continue to see increased visits monthly in 2023 and 2024, improving from the same month in the previous year. In the three most recent months of data, December, January, and February, Aldi, benefitting from its much larger footprint, saw increased year-over-year (YoY) monthly visits of 20.3%, 19.2%, and 28.5%, respectively.

Concentrated on the East Coast, Lidl has seen a smaller increase in visits each month since February of 2023 over the prior year, with the exception of January 2024. February 2023 and February 2024 were the most successful months for YoY visit increases for Lidl at 9% and 8.6% respectively.

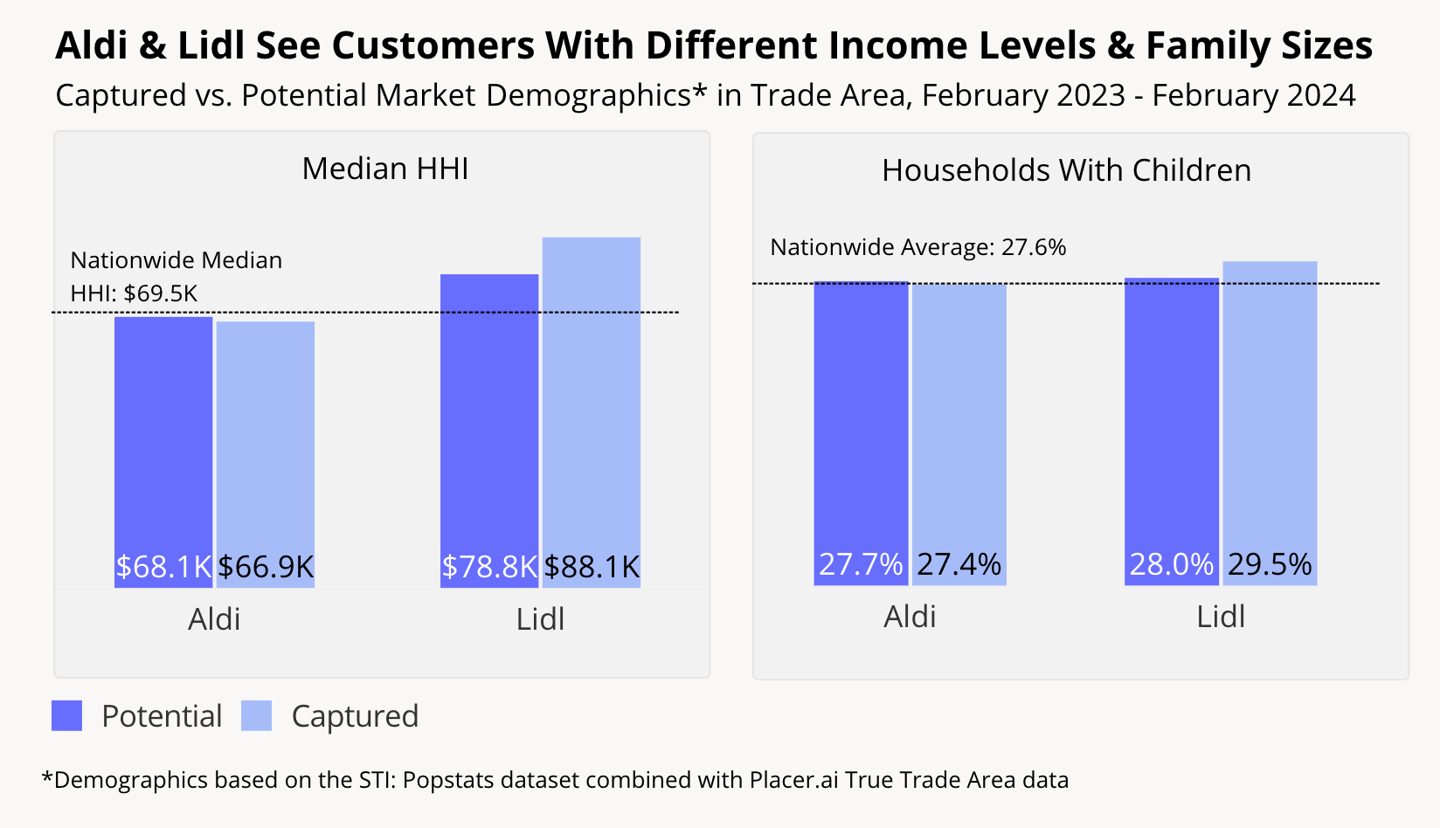

While both grocers are known for their low prices and large selection of private label products, Placer.ai found that the two grocers serve different consumers. The median household income (HHI) in Aldi’s trade area ($68.1K) was slightly lower than the nationwide median, with the median HHI ($69.5K) in the chain’s captured market even lower than the median HHI in its potential market. This shows that Aldi locates its stores in areas that are accessible to the average consumer while succeeding in attracting also the slightly lower income consumers within its potential trade area.

Meanwhile, Lidl’s potential market median HHI ($78.8K) was above the nationwide median, and the median HHI in its captured market ($88.1K) was even higher, indicating that Lidl stores are located in more affluent areas, and that the company caters to the wealthier households within those neighborhoods.

While both brands are popular among suburban audiences, Placer.ai found that Aldi tends to attract a more blue-collar customer, while Lidl is frequented by a wealthier suburban segment. The share of visitors falling into the “Small Town Low Income” category was 7.5% for Aldi, compared to 0.9% for Lidl. Conversely, Lidl saw 16.7% of its visitors falling into the “Upper Suburban Diverse Families” segment, while Aldi had a smaller portion, 10.6%, of its consumers in that category.

“The past few years have seen the grocery space adapting to an increasingly value-oriented consumer, and Aldi and Lidl have benefitted from this shift,” said Bracha Arnold, content writer for Placer.ai. “As inflation cools and both companies expand their footprints, will they continue on their upward trajectory?”

Aldi operates more than 2,200 stores in 38 states, while Lidl operates more than 170 stores in the U.S. across nine East Coast states and Washington D.C.