Resolving excess inventory over the holiday season—and beyond

With the worst of the COVID-19 pandemic—and its social and economic side effects—seemingly behind us, retailers are anxious to rebound during what we can expect to be the most robust holiday shopping season in three years.

On the plus side, ocean freight costs are settling toward near pre-pandemic levels, thanks to stabilizing oil prices, improved capacities at inbound ports, and a general normalization of consumer demand.

However, lower costs have yet to translate into reliability, as on-time performance among the world’s major shipping lines continues to lag below 50%, versus 80% prior to 2020 according to September data from Sea-Intelligence.

When retailers worry whether “their ship will come in” (literally), they compensate by continuing to place advance orders for as much pre-season merchandise as suppliers might promise. The results are gluts of mistimed inventory—which, combined with rising inflation and pivoting consumer spending habits—spiraled into a perfect storm that’s battered most of the retail landscape.

Until recently, the demand and consumer sentiment remained high despite rising inflation. It felt like all product demand was inelastic to price increases. However, the recent Q3 earnings have started showing the pressures of inflation on buying patterns. With credit card debt at a 20-year high, and inflation yet to be cooled down, we are entering into an interesting holiday season that will be challenging for many retailers.

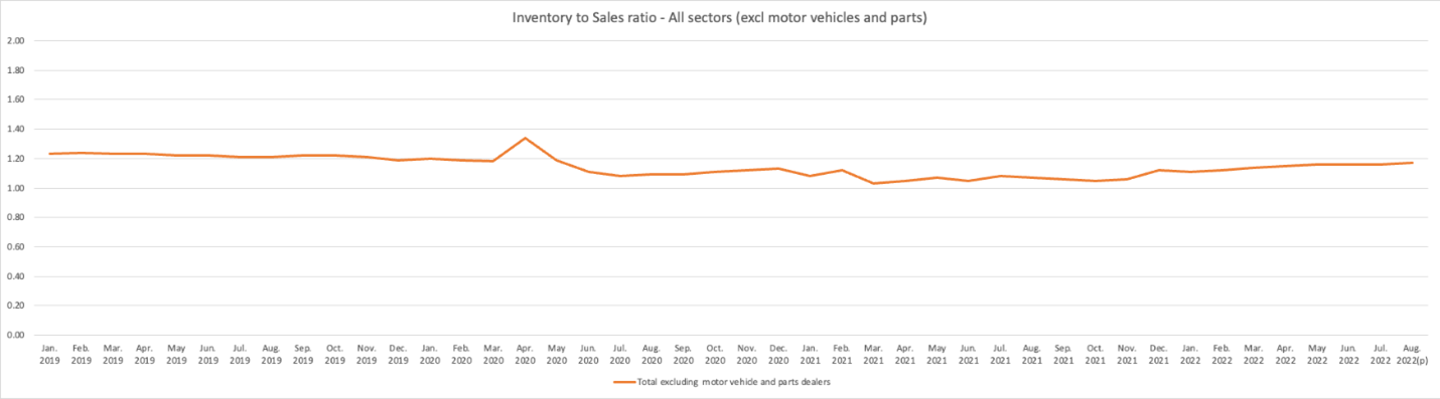

Proof in the numbers

According to benchmark U.S. Census statistics, the average adjusted total inventory across retail for June/July/August timeframe over the past four years has steadily trended upward to $548 million in 2022 from $409 million in 2018.

Effects of excess inventory can be tracked across several retail sectors:

- Building materials and garden supplies appear to currently bear the brunt of the impact, with inventory levels in August 2022 50% higher than pre-pandemic as interest rate increases cool the housing market and post-lockdown consumers look toward travel and other outside experiences over gardening and home upgrades. This trend extends into big-ticket household items such as furniture and large appliances, estimated at almost $32.3 million as of August 2022.

- General merchandise inventory in August 2022 is over 36% more than pre-pandemic levels—an all-time high—long after the frenzied shortages of early 2020. We can anticipate retailers’ strong promotional and markdown pricing in this sector over the coming months to finally move products out the door, impacting their earnings. In many cases, a systematic, analytical approach to forecasting, buying, and promotions could have avoided looming inventory imbalances.

- Clothing & accessories may have seen the earliest out-of-season inventory gluts but have generally done a consistent job of restoring favorable inventory-to-sales ratios, on average lower than pre-pandemic levels, despite the challenges of inflation thanks in large part to aggressive, data-driven pricing and markdown strategies. Department stores, on the whole, have likewise been trending upward and are increasingly poised to maintain right-sized inventories into the holiday season and beyond.

- One notable exception to the excess inventory crisis is the motor vehicle & parts sector, still plagued by materials and supply chain issues, resulting in a 20% inventory shortage. New car prices likely won’t drop anytime soon.

Back to the future

On the whole, there’s much reason for retailers to be cautiously optimistic heading into the crucial holiday season of 2022, but the early signs are not promising. Supply chain disruptions slowly but surely continue to ease, suppliers’ fill rates are becoming more reliable, and logistics costs are trending downward.

Yet a slew of uncertainty remains. Abrupt changes in COVID-19 policies in Asia could quickly impact global commerce, as may the wavering conflict in Eastern Europe. At home, corrective interest rate hikes by the Federal Reserve can prove “bitter medicine” in the short term, alarming stock traders and retail consumers alike. Could the 2022 holiday shopping season be an economic “last hurrah” before an approaching recession we’re being warned about?

Meanwhile, labor shortages continue to hinder every point along the retail value chain, from interstate trucking routes to the regional distribution centers to the local sales floor. We see a slowdown in blue-collar and tech jobs due to market corrections, but the services economy remains vibrant – we have more jobs than there are people wanting to work which continues to pressure retailers.

With so many external variables out there, retailers can still focus on proactive measures they can control—namely, looking ahead toward adopting advanced, data-driven forecasting tools to keep a step ahead of shifting consumer demand, accurately allocating goods across every sales channel, and automated lifecycle pricing to preserve the highest margin from every SKU.

In today’s capricious economic climate, these leading-edge technical solutions are steps retailers can take today toward becoming “disruption-proof” and maintaining their advantage in an ever-competitive marketplace.